Investors are betting the U.S. currency has further to fall as the Federal Reserve nears the end of its most aggressive program of interest-rate increases since the 1980s. Also weighing on the dollar: concerns over the banking system, a potential U.S. debt default and expectations, shared by many economists, that the U.S. will slip into recession in the coming months.

Fed tightening spurred a historic rally in the dollar last year that sent it to multidecade highs against currencies such as the euro and the yen. The dollar began weakening in the fall, held its ground in the new year as inflation proved more stubborn than expected, and has resumed its downdraft in the past two months.

The Fed is expected this week to deliver its last quarter-point rate increase before hitting pause on policy tightening. That would put the Fed at odds with other major central banks, including in the eurozone and the U.K., which reopened from pandemic lockdowns later than the U.S. and are now seeing stickier inflation.

“The U.S. is coming out of a period of extraordinary outperformance. Other countries are starting to catch up,” said

Nick Wall,

head of global foreign-exchange strategy at J.P. Morgan Asset Management.

A weaker dollar is typically good news for the global economy. It lowers the cost of servicing or repaying dollar debt for foreign companies and governments, boosts the value of overseas earnings by U.S. multinationals and can bolster global trade, because goods priced in dollars become more affordable to international buyers.

“It’s a release valve for global growth,” said Mr. Wall. “Sixty percent of global liabilities are denominated in dollars; a lot of those are in emerging markets, and emerging markets are responsible for maybe two-thirds of global growth in the last decade.”

Investors are betting the Fed will pivot to lowering borrowing costs by at least a quarter point by the end of the year,

CME Group

data shows. Meanwhile, market pricing suggests that investors expect the European Central Bank and the Bank of England to raise their key rates by more than half a percentage point by year-end.

That divergence should help currencies such as the euro and British pound to keep gaining against the dollar, analysts say. Rate differentials are a crucial driver of currency markets, as higher rates draw investors in search of yield.

One complication is that the dollar remains a favored asset in times of crisis. If a global recession became a real risk—if, for example, global banking strains worsened markedly—the greenback would likely rally, as happened in early 2020.

Meanwhile, economic momentum is shifting. European growth is holding up unexpectedly well, as the region’s energy crisis has eased, while U.S. activity is slowing. China’s economy expanded by an unexpectedly large 4.5% in the first quarter from a year earlier.

The International Monetary Fund expects the expansion in U.S. gross domestic product to slow to 1.1% next year and eurozone GDP to rise 1.4%, while it sees Chinese growth at 4.5%.

“The dollar-exceptionalism story is weaker not just from the rates perspective, where rates may have peaked, inflation may have peaked well ahead of the eurozone and the rest of the world, but also from a growth perspective,” said

Federico Cesarini,

head of developed-market foreign exchange at

Amundi

Institute.

Mr. Cesarini said rising European interest rates were a “regime shift” for the currency market that could lead to a multiyear dollar downturn. Investors have shunned European bonds since the ECB introduced negative rates in 2014. Now, they are coming home.

“This is really just the beginning,” he said. “I strongly believe a lot of capital from eurozone guys will have to be repatriated back.”

He estimates that about 300 billion euros, equivalent to some $331 billion, has poured back into Europe since last June, mostly into European shares, and that flows could ultimately total about €2 trillion. Amundi forecasts a further 7% rise in the euro this year, to $1.18 from $1.10.

SHARE YOUR THOUGHTS

What is your outlook on the dollar? Join the conversation below.

Hedge-fund managers have been adding to bets against the dollar, which rose to around $12.2 billion as of April 25, according to a Scotiabank analysis of Commodity Futures Trading Commission data. Among those is

Stanley Druckenmiller,

who said last week that shorting the dollar is his only high-conviction trade.

“The one area I feel reasonably comfortable in is, I’m short the U.S. dollar,” Mr. Druckenmiller said at an investment conference hosted by Norway’s sovereign-wealth fund. “Currency trends tend to run at least two or three years. We had a long one here, over $10 trillion came into the U.S. dollar during the previous decade.”

Some say an almost decadelong run-up has left the dollar heavily overvalued.

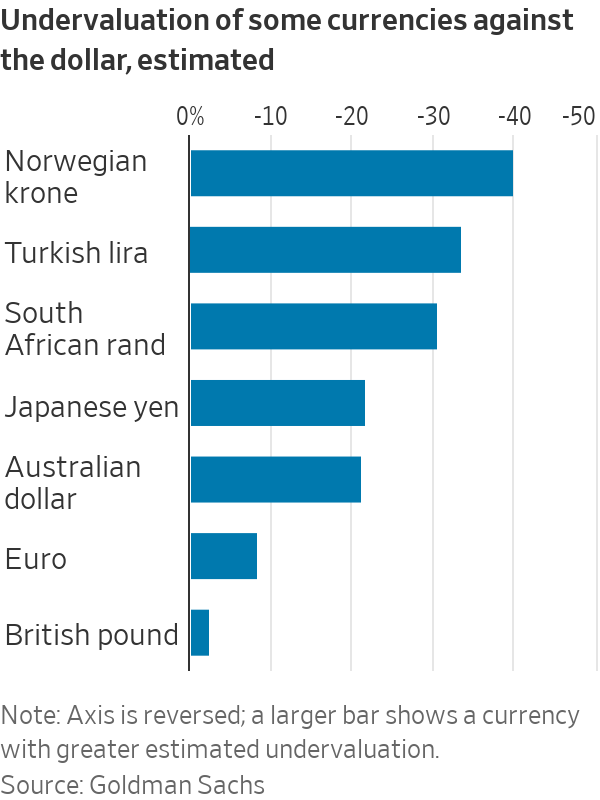

Goldman Sachs

Group Inc. analysts estimate that the currency is between 5% and 15% above its fair value, while other currencies such as the yen, South Africa’s rand and Norway’s krone are sharply undervalued.

History suggests dollar weakness could prove short-lived. In the Fed’s past four rate cycles, the dollar typically weakened or traded flat for three to four months after the final rate increase, before eventually resuming its strengthening,

JPMorgan

Chase & Co. strategists found.

“When you look at the long-term trends, I continue to be relatively favorable on the dollar,” said

Joseph Lewis,

head of corporate hedging at Jefferies. “Big picture, the U.S. still has this dynamic environment that is drawing capital flows.”

Write to Chelsey Dulaney at chelsey.dulaney@wsj.com

Corrections & Amplifications

The dollar has fallen about 8.6% from a peak in September. An earlier version of this article incorrectly said in a photo caption that the dollar had fallen about 8.8% from a September peak. (Corrected on May 1)